Introduction

Real estate has long been considered one of the most reliable investment vehicles. However, traditional real estate investment is often riddled with high entry barriers, a lack of transparency, and time-consuming processes. These inefficiencies have created a demand for innovation—enter Artificial Intelligence (AI) and blockchain technology. Together, these two emerging technologies are transforming the way real estate investments are made, managed, and optimized, making the industry more accessible, efficient, and secure.

Understanding the Core Technologies

What is Artificial Intelligence in Real Estate?

Artificial Intelligence (AI) in real estate refers to the use of advanced algorithms and machine learning models to analyze large volumes of data, predict trends, and automate processes. From evaluating property values and predicting market shifts to managing buildings and tenant relations, AI enhances decision-making and reduces the reliance on manual tasks. Its predictive analytics capabilities enable investors to identify lucrative opportunities with more accuracy and less risk.

What is Blockchain in Real Estate?

Blockchain is a decentralized digital ledger technology that records transactions across multiple systems in a way that ensures the data cannot be altered retroactively. In real estate, blockchain facilitates transparency, reduces fraud, and automates transactions through smart contracts. It also supports the tokenization of assets, enabling fractional ownership and increased liquidity in the market. Together with AI, blockchain brings a new level of trust and efficiency to real estate investment.

The Traditional Real Estate Investment Landscape

High Barriers to Entry

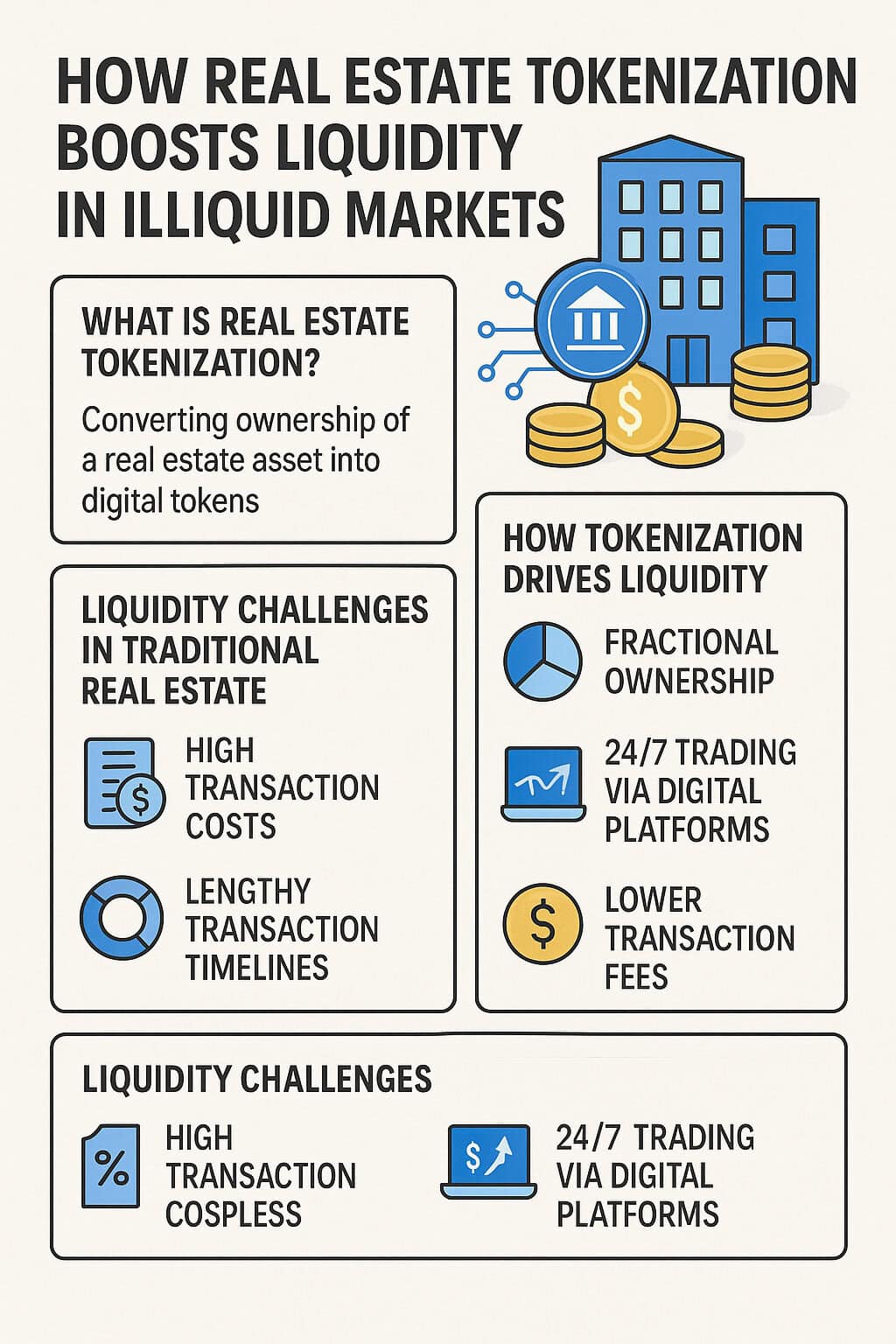

Historically, investing in real estate has required substantial capital, making it inaccessible to many individual investors. Beyond financial barriers, the process of buying, selling, or leasing property involves layers of legal documentation, third-party verification, and prolonged negotiation periods. These obstacles can deter new investors from entering the market.

Lack of Transparency and Trust

The conventional real estate market often suffers from opacity. Property history, title authenticity, and transaction records are not always easily verifiable, creating room for fraud and misrepresentation. This lack of trust can increase due diligence costs and reduce investor confidence.

Inefficiencies in Property Management and Transactions

Traditional property management and real estate transactions involve significant manual intervention—from tenant screening and rent collection to maintenance and legal compliance. Additionally, property sales and transfers can take weeks or even months, primarily due to the involvement of multiple intermediaries and cumbersome verification processes.

These foundational issues underscore the need for technological innovation, setting the stage for AI and blockchain to revolutionize the real estate investment space.

How AI is Transforming Real Estate Investment

Predictive Analytics for Property Valuation

One of AI’s most transformative applications in real estate lies in predictive analytics. By analyzing large volumes of structured and unstructured data—such as historical pricing, market demand, interest rates, and neighborhood trends—AI models can forecast future property values with remarkable accuracy. Investors benefit from a deeper understanding of potential risks and rewards, enabling smarter buying, selling, and leasing decisions.

AI-Powered Risk Assessment

Traditional risk assessments are often time-consuming and rely on outdated or incomplete data. AI revolutionizes this process by instantly evaluating an investor’s profile, creditworthiness, market volatility, and even macroeconomic indicators. AI algorithms can flag anomalies and detect potential fraud patterns early, ensuring safer transactions and reducing losses for both lenders and investors.

Intelligent Property Management Systems

AI is also streamlining property management through automation and intelligent systems. Tools such as AI-powered chatbots handle tenant inquiries, schedule maintenance, and even assist with lease renewals. Predictive maintenance systems can alert landlords to potential issues before they become costly repairs. Tenant screening algorithms evaluate application data to identify high-quality renters, enhancing occupancy rates and reducing turnover.

Blockchain’s Role in Real Estate Investment

Smart Contracts for Secure Transactions

Smart contracts are self-executing contracts with the terms of the agreement written directly into code. In real estate, they eliminate the need for intermediaries such as brokers, lawyers, and escrow agents. Once predefined conditions are met—like payment or verification of ownership—the contract automatically executes the transaction. This not only reduces costs but also accelerates the closing process while ensuring security and trust.

Tokenization of Real Estate Assets

Blockchain enables the tokenization of real estate, breaking down properties into digital tokens that represent fractional ownership. This innovation lowers the financial barrier for entry, allowing a broader range of investors to participate in real estate markets. Investors can buy, sell, or trade these tokens on digital exchanges, boosting liquidity and flexibility compared to traditional real estate investments.

Immutable Records and Enhanced Due Diligence

Blockchain’s inherent transparency and immutability make it ideal for maintaining accurate and tamper-proof records. Title deeds, ownership history, and transaction logs can all be securely stored on a blockchain, simplifying the due diligence process. This eliminates the risk of forgery and enhances buyer confidence, significantly streamlining legal and compliance procedures in property transactions.

Synergy of AI and Blockchain in Real Estate

Automated and Transparent Investment Platforms

When AI and blockchain converge, they form highly automated and transparent real estate investment platforms. AI handles data processing and decision support, while blockchain ensures data integrity and security. These platforms can onboard users, verify credentials, analyze properties, and execute transactions autonomously, offering a seamless and efficient user experience.

Enhanced Decision-Making with Verified Data

Blockchain’s ability to store verified, immutable data feeds directly into AI models, enhancing the quality and reliability of analytics. With accurate historical records and real-time data, AI can generate more nuanced and dependable investment insights. This synergy empowers investors with superior tools for evaluating opportunities, mitigating risks, and optimizing portfolios.

Benefits for Investors

Lower Barriers to Entry

AI and blockchain are breaking down long-standing financial and operational barriers in real estate. Tokenization enables fractional investments, allowing individuals to invest in high-value properties with minimal capital. AI streamlines onboarding and evaluation processes, making it easier for first-time investors to enter the market with confidence.

Higher ROI Potential

With AI delivering powerful analytics and insights, investors can identify high-potential properties and optimal investment timings. Blockchain minimizes transaction fees and intermediaries, preserving more of the investment’s value. Together, they contribute to more profitable and efficient investment outcomes.

Global Investment Opportunities

These technologies transcend geographical limitations. AI can analyze global market trends, while blockchain ensures secure, transparent cross-border transactions. As a result, investors can diversify their portfolios internationally, accessing markets that were previously difficult to enter due to regulatory or logistical hurdles.

Challenges and Limitations

Regulatory Hurdles

The integration of AI and blockchain into real estate investment is not without legal and regulatory challenges. Many jurisdictions have yet to fully recognize the legal status of smart contracts and tokenized assets. Moreover, data privacy regulations may restrict the kind of information AI systems can access. Navigating these regulatory landscapes requires collaboration between technologists, policymakers, and legal experts.

Technology Adoption and Integration

Despite their potential, AI and blockchain face adoption hurdles in the traditionally conservative real estate industry. Legacy systems, lack of technical expertise, and resistance to change can impede integration. In addition, the interoperability between different blockchain platforms and the quality of available data for AI training remain significant technical concerns that must be addressed for seamless adoption.

The Future of Real Estate Investing with AI and Blockchain

Emerging Trends and Innovations

The intersection of AI and blockchain is giving rise to cutting-edge trends like AI-powered real estate token marketplaces, decentralized autonomous organizations (DAOs) for property management, and the integration of real estate into the metaverse. These innovations offer new forms of ownership, interaction, and profit-generation for digital-native investors.

Predictions for the Next Decade

Over the next ten years, we can expect a more democratized and global real estate market. Blockchain will facilitate borderless property investments while AI continues to improve accuracy in risk assessment and predictive valuations. Governments may begin to adopt regulatory frameworks to support this transformation, and institutional investors will likely increase their participation in tech-powered real estate platforms.

Conclusion

AI and blockchain are not just buzzwords—they are foundational forces reshaping real estate investing. From lowering entry barriers and enhancing transparency to unlocking new global markets, these technologies are creating a smarter, more inclusive, and more efficient investment landscape. As adoption grows and innovation accelerates, investors who embrace these tools early will be best positioned to benefit from the evolving future of real estate.

FAQs

What is real estate tokenization?

Real estate tokenization is the process of converting property ownership into digital tokens that can be bought, sold, or traded on blockchain platforms. Each token represents a fractional share of the asset, enabling broader investor access.

Can AI predict real estate market trends?

Yes, AI uses historical data and real-time analytics to identify patterns, forecast market movements, and assess the potential value of properties, helping investors make informed decisions.

Are blockchain-based transactions legally binding?

In many jurisdictions, smart contracts are gaining legal recognition. However, their enforceability varies globally and often depends on local laws and how the contract terms are structured.

How secure are smart contracts?

Smart contracts are generally secure due to blockchain encryption and immutability. However, they are only as reliable as their code, which must be properly audited to avoid vulnerabilities.

Is it safe to invest in AI-powered real estate platforms?

AI-powered platforms can offer enhanced decision-making and risk assessment, but like any investment, they carry risks. It’s important to conduct due diligence and consider platform credibility, regulatory compliance, and technology maturity.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}